The New Frontier: Private Equity’s Influence on Accounting

The accounting profession stands at a crossroads. Recent acquisitions of second-tier accounting firms by private equity groups signal a shift that could redefine the industry’s future.

In February 2024, US accounting firm Baker Tilly agreed to sell a majority stake to Hellman & Friedman and Valea. A month later, the US arm of accounting firm Grant Thornton has agreed to sell a majority stake to the investment group New Mountain Capital.

A Tradition of Trust

Accounting has traditionally been a profession grounded in trust; at least, this was what was drilled into us when I qualified as a chartered accountant in England years ago.

Accountants are the gatekeepers of capitalism. They ensure financial statements reflect a company’s financial health and underpin credit and investment decisions by vendors, bankers and investors. This trust is the cornerstone of the profession’s proud legacy.

The Winds of Change

However, the landscape is changing. Private equity’s foray into accounting, exemplified by the recent acquisitions of two notable second-tier firms, raises questions about the future. These moves are not isolated incidents but part of a broader trend where private equity sees potential in the steady, reliable returns that accounting firms can offer.

The Private Equity Proposition

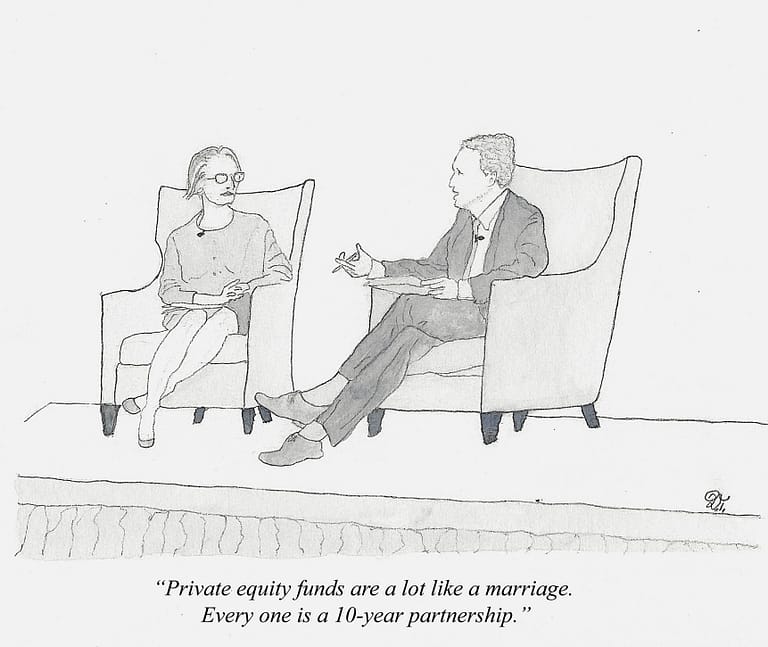

Private equity groups bring capital, business acumen, and a drive for efficiency. They promise innovation, growth, and a path to rapid scaling that traditional models cannot match. But at what cost? The profession’s ethos of putting truth above profits may be challenged as these investors seek investment returns.

Would an accounting partner walk away from subtle client pressure to sign off on accounts that flatter sales and profits, knowing the impact on fees and profit? Client pressure exists under the partnership model today, and the profession’s track record has not always been great (Enron et al.). What would happen when more accounting firms are owned by private equity, which demand a 2-3x return in 5 years?

The Future of the Partnership Model

As more accounting firms align with private equity, the profession may witness a transformation. The partnership model, which prioritizes collective decision-making and long-term client relationships, might give way to corporate structures emphasising efficiency and profit.

The question remains: Can the accounting profession maintain its foundational principles in this new era? Or will the relentless pursuit of profit erode the trust that has been its hallmark? Should regulators step in for the sake of public good?

The New Frontier: Private Equity’s Influence on Accounting Read More »